Taxes help fund the services and infrastructure that make Duck a safe, vibrant, and welcoming town. Here you can find information about property taxes, how they are calculated, and where your tax dollars go.

Please note that the Town of Duck contracts with the Dare County tax office to collect our taxes. This enables our residents to receive one tax bill and remit payment to one place. If you have any questions related to your tax bill, please contact the Dare County Tax Department at 252.475.5940.

CURRENT TAX RATES

Fiscal Year 2025-2026

| Town of Duck | 0.1800 |

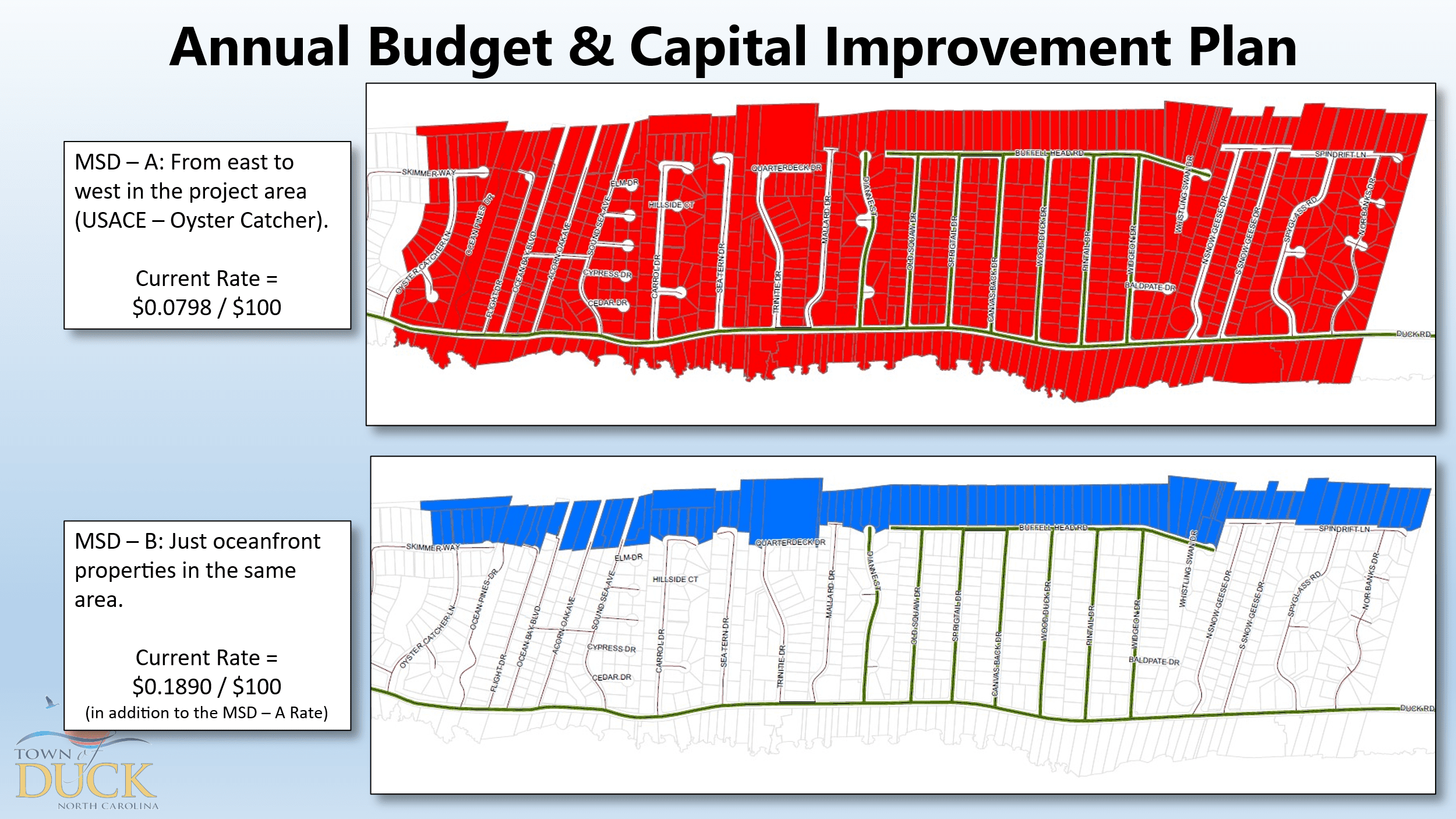

| Beach Nourishment- MSD A (All properties from the US Army Corps of Engineers to Oyster Catcher Lane) | 0.0798 |

| Beach Nourishment- MSD B (Only oceanfront properties from US Army Corps of Engineers to Oyster Catcher Lane) | 0.1890 |

Click here to view a map of the MSD Districts.

{kind=link}

TYPES OF TAXES

Learn about the various taxes below. Please refer to the Fiscal Year 2025- 2026 Budget Document for more information.

Property taxes in Duck are based on the value of real property, personal property, and motor vehicles. “Ad Valorem” is a Latin term meaning “according to value,” which reflects how taxes are calculated. The tax base includes:

- Real property: land, buildings, and improvements

- Personal property: boats, business equipment, and other belongings

- Property of public service companies: electric, telephone, and railroads

- Automobiles

When property values are updated through revaluation, North Carolina law requires the Town to calculate a revenue-neutral tax rate. This rate shows what the tax rate would need to be to generate the same total revenue as before the revaluation, providing a benchmark for taxpayers.

Key points:

Key points:

- The revenue-neutral rate helps property owners compare the proposed tax rate after revaluation.

- Even if the official tax rate is lowered, property owners may still see an effective increase depending on changes in property values.

-

- Determining the rate that would produce the same revenue as the current year.

- Adjusting for average growth in the tax base from improvements.

- Accounting for annexations, deannexations, or mergers (not applicable in Duck).

In addition to the Town-wide property tax, Duck has two Municipal Service Districts (MSDs). These districts collect a separate tax on properties within their boundaries, and the revenue is dedicated solely to beach nourishment projects.

Key points:

This approach ensures that MSD funds are used efficiently while maintaining long-term access and upkeep of Duck’s beaches.

Key points:

- MSD-A covers all properties in the project area; MSD-B covers only oceanfront properties.

- Tax rates are set to cover debt service for nourishment projects and are updated each year during budget preparation.

- In FY 2020-21, MSD-A’s rate was $0.1296 and MSD-B’s was $0.285. The current draft budget sets rates at revenue-neutral levels: MSD-A $0.0798 and MSD-B $0.1890.

- Recent renourishment work was completed in spring 2023, and current modeling shows no need to increase MSD rates for upcoming debt service.

- Future rates may change depending on debt requirements for future nourishment projects, including the next cycle in 2027.

This approach ensures that MSD funds are used efficiently while maintaining long-term access and upkeep of Duck’s beaches.

Duck receives revenue from two main types of taxes collected by the State:

Key points:

- Sales Tax: Charged on retail sales, leases of tangible property, and hotel/motel rentals.

- Use Tax: An excise tax on using or consuming property in North Carolina or elsewhere.

Key points:

- The Town tracks sales and use tax trends and attends economic briefings to anticipate changes in revenue.

- Revenue grew during the pandemic years but is showing a small decrease in FY 2024-25. The Town budgets conservatively to account for economic unpredictability.

- Restricted funds: About 17.7% of Duck’s sales tax revenue is dedicated to beach nourishment projects, in line with the Municipal Service Districts’ purpose.

North Carolina law requires an excise tax on certain real estate transfers. In Dare County, the tax is $1 for every $100 (or fraction thereof) of the property’s sale price.

Key points:

Key points:

- Revenue is restricted by law for capital projects or debt service, including courts, jails, EMS, libraries, recreation, education, water and sewer, health, and social services. Municipalities must also use their share for capital projects or related debt.

- After the first twelve years, 35% of the tax revenue is distributed to towns based on each town’s share of property taxes, with Dare County retaining 65%.

-

- FY 2020-21 and FY 2021-22 saw record collections due to a strong real estate market.

- FY 2023-24 experienced a decline.

- FY 2024-25 shows a small increase, but the Town budgets conservatively, assuming activity similar to the previous year.

Dare County levies a 6% occupancy tax on gross receipts from rentals of rooms, lodging, campsites, or similar accommodations, including private residences and cottages rented to transients. This tax does not apply to rentals under 15 days per year or stays of 90 or more consecutive days.

The revenue is shared between the County and towns and is restricted by law for specific purposes:

3% Room Occupancy Tax – Tourism & Public Services

The revenue is shared between the County and towns and is restricted by law for specific purposes:

3% Room Occupancy Tax – Tourism & Public Services

- Used for tourist-related public services such as facility maintenance, garbage collection, police, and emergency services.

- Two-thirds goes to the six towns, including Duck, based on each town’s property tax share.

- Duck uses its portion as collateral for Special Obligation Bonds for beach nourishment.

- 75% funds administration and tourism promotion (marketing, events, hospitality programs).

- 25% funds services or programs needed due to tourism impacts.

- Funds costs related to beach nourishment projects, including construction, permits, public access improvements, dune restoration, and sand placement.

- FY 2023-24 revenue was nearly level with the prior year.

- FY 2024-25 is expected to be slightly higher than budget but reflects a moderation in reservation numbers.

- The Town budgets conservatively, anticipating stable revenue without expecting significant growth.

The State collects license and excise taxes on liquor, beer, and wine, with a portion of these taxes shared with cities and counties that allow sales within their limits.

- Beer: 23.75% of the excise tax is distributed to local governments.

- Unfortified Wine: 62% of the excise tax is shared.

- Fortified Wine: 22% of the excise tax is shared.

The Town of Duck receives revenue from three related tax sources: electricity and natural gas sales tax, video programming tax, and telecommunications tax.

Electricity and Natural Gas Sales Tax

-

- A portion of the state general sales tax on electricity and natural gas is returned to municipalities.

- Duck receives 44% of electricity tax proceeds, ensuring at least the same revenue as FY 2013.

- FY 2023-24 revenue from this source was $422,005.

-

- Local cable franchise fees were replaced with a statewide system in 2007.

- The shared pool comes from taxes on telecommunications services, video programming, and satellite services.

- Revenue is distributed after funding public access, based on population.

- FY 2023-24 revenue from this tax was $27,697.

-

- Revenue comes from a statewide pool based on prior franchise fees.

- Our share remains constant, but the pool can fluctuate.

- Revenue is declining statewide due to fewer landline phones.

- FY 2022-23 revenue from this tax was $3,015.

- FY 2024-25 budgets reflect a small increase over prior year estimates for these combined taxes.